Back to: ECONOMICS SS1

Welcome to class!

In today’s class, we will be talking about the equilibrium price. Enjoy the class!

Equilibrium Price

A free market is a market in which prices of goods and services are regulated by market forces. This means that prices of commodities in a free market economy are fixed by the interaction (i.e. joint actions) of demand and supply.

Determination of prices in a free market

It is possible to compare demand with the supply by drawing a schedule showing the number of goods demanded and supplied. An example of a combined demand and supply schedule is shown below.

Price N Quantity Demanded (Units) Quantity Supplied (Units)

7 100 900

6 200 700

5 300 650

4 400 400

3 500 300

2 600 250

1 700 200

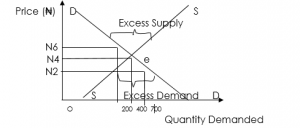

The schedule above can be graphically represented by the curve below.

From the table and graph above, it is seen that at N4, 400 units of goods were demanded and 400 units of goods were supplied. N4 is the equilibrium price, while 400 units are the equilibrium quantity and the point of intersection between the demand curve and the supply curve is called the equilibrium point.

Equilibrium point, equilibrium price and equilibrium quantity

Given a downward-sloping demand curve and an upward-sloping supply curve as in the diagram above, there would occur a unique point of intersection indicating a price level at which quantity supplied will be equal to the quantity demanded. Such point of intersection is called an equilibrium point, and when such point is traced to the price and quantity axis of the graph, we shall obtain the equilibrium price and equilibrium quantity bought and sold respectively. From the graph above, the equilibrium point was established at point A, and when traced to the price and quantity axis, it showed the market equilibrium price and equilibrium quantity bought and sold of N4 and 400 units respectively. The equilibrium price is the price at which the number of goods demanded is equal to the quantity supplied. This price is determined by the interaction of supply and demand

At a price, lower than the equilibrium price (say N2) demand will be greater than supply. This will lead to a shortage of goods in the market that is, excess demand. On the other hand, at a higher price than the equilibrium price (say N6), producers will supply more than the consumers are willing to buy and this will lead to an excess supply – i.e surplus of goods in the market.

Derivation of equilibrium price and quantity from demand and supply functions

Given the Demand and supply functions:

Qd = 42-2p and Qs =12+4p

Determine the equilibrium price and equilibrium quantity

Solution

At equilibrium price

Qd = Qs

i.e. 42- 2p = 12+4p

42-12 = 4p +2p

30 = 6p

P= 30/6 = 5

Equilibrium price = N5

To obtain the equilibrium quantity

Substitute for p in

Qd = 42 –2p

Qd = 42 – 2 (5)

= 42 –10

= 32

Equilibrium Quantity = 32units

Evaluation

- What is equilibrium position?

- Describe the condition for equilibrium.

- What is the equilibrium quantity?

- Illustrate with a diagrammatic sketch the market situation at a price lower than the equilibrium price

- Explain the term “market forces”

- “Prices are determined by the forces of demand and supply”. Explain and illustrate with a diagram.

Price system or price mechanism

Meaning of a price

Price is defined as a monetary unit of measurement or value that helps to facilitate the exchange of goods and services in the market. That is, a price is a rate at which something can be exchanged for another thing. For goods to command a price, it must have the attributes of usefulness (valuable) and relative scarcity.

Price system or price mechanism

In a free-market economy, prices of goods and services affect the behaviour of both the consumer and the producer (supplier). Price system may be defined as a system whereby prices of goods and services are determined by the free interaction of the forces of demand and supply in a free market economy. That is, it is a system of resources allocation based on a free movement of prices. It is described as a process by which the monetary value of a commodity, service, or factor of production is determined by the interplay of the market forces of demand and supply.

Functions/importance of the price system

- The price system operates to allocate scarce resources

- It regulates the flow of goods and services from producers to the consumer.

- It determines the extent of demand and supply of goods and services.

- It is used to encourage or discourage the consumption of certain goods and services.

- It helps to determine how the factors of production will be rewarded.

Evaluation

- Define price mechanism.

- List the importance of a price mechanism.

Factors that determine the price of commodities

- The cost of production of the product

- The level of profit desired by the seller

- The level of competition in the market

- Government policies e.g. subsidies, taxation etc.

- The activities of Trade Unions

- The cost incurred on advertisement

- Changes in demand and supply

Price fixing methods

The prices of goods and services are often fixed by any of the following methods:

- Through Bargaining System

- Through Sales by Auction

- Through Sales by Price Tags

- Through Market Forces of Demand and Supply

Evaluation

- Explain factors that determine the price

- State three price-fixing methods

Reading assignment

- Amplified and Simplified Economic for SSS by Femi Longe page 290–296

- Fundamentals of Economics by Anyawuocha page 166-168

General evaluation questions

- Distinguish between fixed cost and variable cost.

- Under what condition will a perfectly competitive firm maximize profit.

- Describe each of the following: (a) abnormal demand (b) effective demand

- What is a public corporation?

- Explain the causes of a declining population.

Theory

- Given the demand and supply function for a crate of eggs as follows: Qd = 12 –2p; Q = 3+1p

- Determine the equilibrium price and quantity

- What is the excess supply at the price of N3.50?

- State three factors that determine the price of commodities

In our next class, we will be talking about the Nature of Nigeria Economy. We hope you enjoyed the class.

Should you have any further question, feel free to ask in the comment section below and trust us to respond as soon as possible.