Back to: FINANCIAL ACCOUNTING SS1

Welcome to today’s class. We will be talking about the meaning and types of accounting concepts and conventions.

Accounting Concepts and Convention

By the end of the lesson, you should be able to;

- Write out accounting concepts and conventions

- Distinguish between accounting concepts and conventions

- Justify the needs for accounting concepts and conventions

Accounting concepts and conventions are a set of rules or principles that are taken into consideration in the preparation of financial statements. The financial statements include Trading, profit and loss account as well as the balance sheet. For uniformity of purpose, generally accepted rules or principles in the form of assumption for its preparation and presentation are adopted, and these are called accounting concepts and conventions.

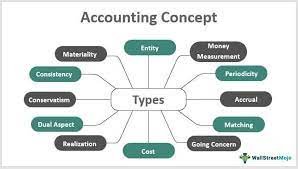

Accounting Concepts

They are the basic or fundamental assumptions on which the financial accounts of a business enterprise are prepared and presented.

The accounting concepts are explained below:

- BUSINESS ENTITY CONCEPT: The rule here is that the owner and the business are treated separately. Therefore in the preparation of the financial statement, the business is recognized as a separate and distinct entity, only things that affect the business are recorded and not the wealth of the owner(s) apart from those invested.

- GOING CONCERN CONCEPT: Going concern means continuity and not liquidation. That is no reason or fear of discontinuity exists.

- MONEY MEASUREMENT CONCEPT: This concept states that financial statements must reflect only transactions and entries that are capable of being expressed in monetary terms.

- COST CONCEPT: In the preparation of financial statements. Assets are valued at cost. It is on cost and not market value because the business is not for sale.

- ACCRUAL CONCEPT: This concept states that expenses and revenue are recognized and reported in the profit and loss account as they are incurred and earned respect and not as they are paid or received.

- MATCHING CONCEPT: This concept explains that all expenses must be matched and reported against revenue generated at that period to determine the net profit. NB: This is the same as the accrual concept

- DUAL ASPECT CONCEPT: This explains the principle of double-entry.

- REALISATION CONCEPT: This concept explains that income is recognized as soon as goods are exchanged for valuable consideration.

Accounting Conventions

They are the generally acceptable approaches to the application of the accounting concepts.

- MATERIALITY CONVENTION: This convention states that amount of materials significant n value must be recorded in the preparation of the financial statement. This explains why certain economic events are not reported when the amount of their value is insignificant as to affect the financial statement e.g. depreciation of calculator, wall clock etc.

- CONVENTION OF CONSERVATISM: The convention of conservatism states that the principles of treating income and losses as well as the valuation of assets.

Income should not be anticipated

All possible losses must be provided for

When more than one method of valuing an asset is evolved, choose the method with less value (i.e. lower of cost) and or market value.

- CONSISTENCY CONVENTION: This states that there should be consistency in the treatment of similar transactions. This implies that similar transactions within the same period and between one period and another must be treated alike, any changes of a method may distort the profit calculation.

In our next class, we will be talking about the Final Account of a Sole Trader. We hope you enjoyed the class.

Should you any further question, feel free to ask in the comment section below and trust us to respond as soon as possible