Back to: FINANCIAL ACCOUNTING SS1

Welcome to class!

In today’s class, we will be talking about the correction of errors. Enjoy the class!

Correction of Errors

CONTENT

- Suspense Accounts

- Correction of Errors

Errors made in the recording of the day-to-day transactions can be divided into those which are not revealed (disclosed) by the trial balance and those which result in the trial balance not balancing.

Where the trial balance total does not agree it is usual to apply the following quick checklist to locate the errors.

- Check the additions of the trial balance.

- Check the addition of the balance of each ledger account.

- Check that each ledger account balance has been entered in the correct column of the trial balance.

- Check that every ledger account balance has been entered in the trial balance.

- Look for a transaction equal to the difference in the trial balance and check that a double-entry has been made for that transaction.

- Look for a transaction equal to half the difference in the trial balance and check if it has been entered twice on the same side of the ledger rather than once on each side.

- Check the double entry for every transaction entered in the books since the date of the last trial balance.

If after applying the above quick checklist the errors are not found immediately, the trial balance is balanced temporarily by inserting the difference between the trial balance totals in a Suspense Account.

The Suspense Account is a temporary account in which the difference in the trial balance is recorded until the errors are located (discovered) and corrected.

Where the trial balance totals do not agree and to avoid any delay in the preparation of the final accounts, a Suspense Account would be opened to record the difference in the trial balance totals pending the time the error(s) are located and corrected. As the errors are found, they are corrected by means of a journal entry (i.e. an entry in the General Journal). The appropriate entries are then made in the ledger accounts. When all the errors have been found and corrected, the suspense account will close automatically.

Uses of the suspense account

- A suspense account is used to record a difference in the trial balance temporarily until the errors are detected and corrected.

- A suspense account is also used when transactions are recorded in the books before any decision has been made about their proper accounting treatment

- The suspense account provides an account to which an entry (i.e. one aspect of a transaction) could be made until its correct destination (i.e. the account to which it should be posted) is known

How to open a suspense account

A Suspense Account is opened in the general ledger with a balance on whichever side of the Suspense Account that will make the trial balance agree when the balance is inserted in it. For example, if the total of the credit side of a trial balance is N6, 000 less than the total of the debit side, the Suspense Account will be opened with a credit balance of N6, 000. When the Suspense Account balance is inserted in the trial balance, the trial balance will balance.

NB: Once a Suspense Account is opened, the final accounts can be prepared even if all the errors have not been discovered. In this, case the balance on the Suspense Account will appear in the Balance sheet (as an asset if it is a debit balance and as a liability, if it is a credit balance).

How to correct errors

The correction of errors will require journal entries which will be posted to the ledger accounts.

- If the error being corrected does not affect the agreement of the trial balance, the journal and ledger entries will not involve the Suspense Account

- If the error being corrected affects the agreement of the trial balance, the journal and ledger entries will involve the Suspense Account

Step (processes) involved in the correction of errors

To decide how to correct an error asks the following questions.

- How should the transaction have been recorded?

- How has the transaction been recorded?

- What type of error has been committed by the book-keeper who recorded the transaction? e. will the error affect or not affect the agreement of the Trial Balance? As indicated above, this step is very crucial to indicate whether the Suspense Account will be involved in the correction of the error or not.

- What entries are required to be passed to correct the error?

In applying the steps enumerated above, it is useful to remember the following.

- An item on the wrong side of an account must be corrected by an adjustment equal to twice the amount of the original error (once to cancel the error and once to place the item on the correct side of the account).

- Some errors do not affect the double-entry: an example would be a debit balance on Rent Account N850 included in the trial balance as debit balance N To correct the error, a one-sided entry should be made in the journal and the Suspense Account. Such errors do not require to be corrected by debit and credit entries.

Evaluation

- Briefly explain three uses of Suspense Account

- State seven errors that will be disclosed by the Trial Balance

Illustration:

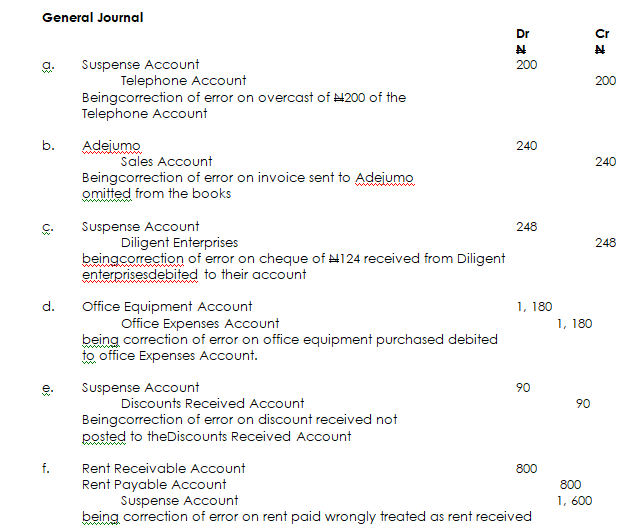

Kehinde extracted a trial balance from her ledgers on 31st December 2017. The trial balance totals were N23, 884 (debit) and N24, 856 (credit). She placed the difference in a Suspense Account. Subsequent

An investigation into the accounts revealed the following:

- The debit side of the Telephone Account had been overstated by N200

- An invoice sent to Adejumo forN240 had been completely omitted from the books.

- A cheque for N124 received from Diligent Enterprises had been posted to the debit of their account

- The purchase of some office equipment for N1,180 had been debited to Office Expenses Account

- Discounts received, N90, had been posted to the purchases ledger but not to the Discounts Received Account.

- Rent paid, N800 had been credited to Rent Receivable Account.

- A refund of an insurance premium, N60, had been recorded in the Cash Book but no other entry had been made.

- Purchase of office stationery, N220, had been debited to Purchases Account in error.

- A credit balance of N30 in the purchases ledger had been omitted from the list of balances extracted from the ledger. The total of the list had been included in the trial balance.

- Goods returned to Ready Stores had been credited to Ready Stores Account and debited to Purchases Returns Account. The goods had cost N400

Required:

- Prepare journal entries to correct the errors indicated above

- Prepare the Suspense Account showing the opening balance and the correcting entries

Evaluation

- Simplified and Amplified Financial Accounting Exercise 2, 3, 4, 5X, 6 and 9

- Essential Financial Accounting Exercise 12.2, 12.5A, 12.8A and 12.9A

Reading assignment

- Simplified and Amplified Financial AccountingPage 134 – 154

- Essential Financial Accounting Page 90 – 105

Weekend assignment

- Which of the following errors will affect the totals of a trial balance compensating errors

- complete reversal of entry C. error of original entry D. omission a ledger balance in the trial balance

- Pending the location of an error, the difference disclosed in a trial balance is temporarily treated in Suspense Account B. Trading Account C. Control Account D. Profit and Loss Account

- Which of the following accounts has a credit balance Cash B. Capital C. Drawing D. Premises

- Purchases Account is overcast by N200, while wages Account is undercast by N200. This is an error of omission B. a compensating error C. an error of commission D. an error of principle

- Which of the following is entered in the General Journal purchases of goods B. sale of goods on credit C. returns inwards D. acquisition of fixed assets

Theory

- What is a Suspense Account

- State three uses of a Suspense Account

We hope you enjoyed the class.

Should you any further question, feel free to ask in the comment section below and trust us to respond as soon as possible.