Back to: FINANCIAL ACCOUNTING SS1

Welcome to class!

In today’s class, we will be talking about opening entries and recording of subsequent financial transactions. Enjoy the class!

Opening Entries and Recording of Subsequent Financial Transactions

CONTENTS:

- Opening Journal entries

- Recording of subsequent financial transactions

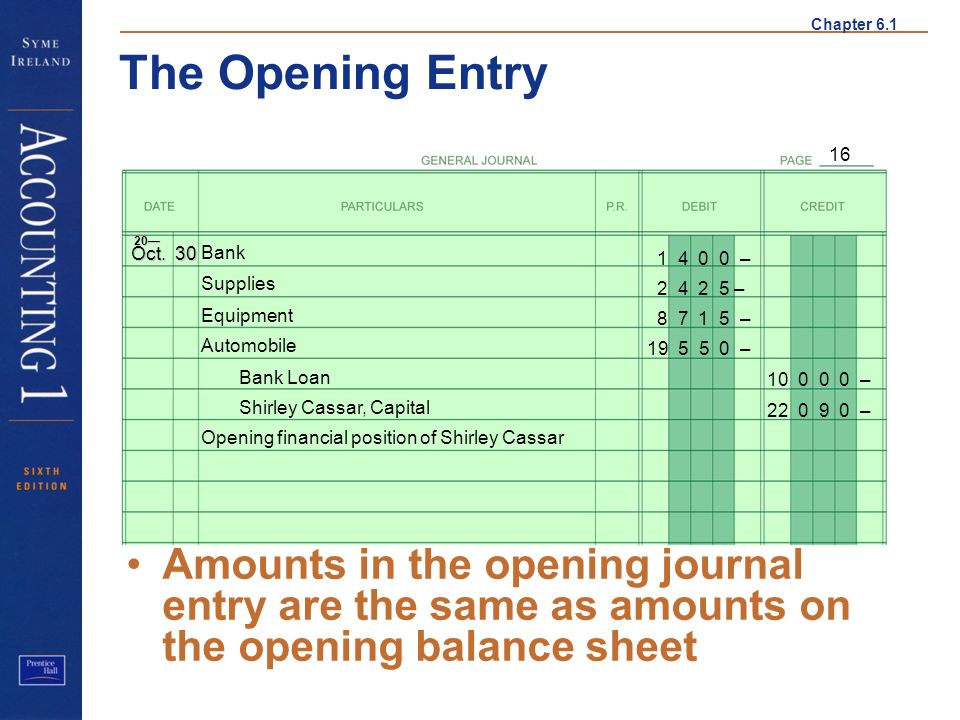

When a business begins the capital will consist of cash, money in the bank and other assets. To record this event, a set of books must be opened. Also, on deciding to keep his books on double-entry principle or on opening a new set of books the trader will record what is known as opening entries. For the three cases identified above, the General Journal (or Principal Journal or Journal Proper) is used to record the opening entries.

The trader will summarizes his financial position. This summary will disclose that he has certain assets, valuable possessions and properties which is to be used in the business. In addition, certain sums of money may be owing to him by customers, while, on the other hand, he may owe various sums. The latter are his liabilities, and, taking the total of these from his assets, he is able to say what he is worth financially. That amount by which his assets exceed his liabilities is called his capital.

The summary as described above is recorded in the General Journal and is known as the opening entries.

Illustration:

William Kamara decides to open a set of books on double-entry principle. His business affairs on 1st July 2017 stand as follows: office cash N13,300; bank balance N27,700; the value of motor vehicles N42,000; a stock of goods N14,200; two debtors Olamide and Victoria owe him N21,800 and N18,000 respectively. He owes two creditors B. Mohammed and S. Talabi, N7,000 and N20,000 respectively.

Required:

Prepare the journal entries to open the books of William Kamara as at 1st July 2017.

General Journal

2017 N N

Jul 1 Cash CB 13,300

Bank CB 27,700

Motor Vehicles GL 42,000

Stock GL 14,200

Olamide SL 21,800

Victoria SL 18,000

Mohammed PL 7,000

Talabi PL 20,000

Capital GL 110,000

being assets, liabilities and capital at this date 137,000 137,000

The items in the above opening entries are then posted to the ledger, the assets being debited to the respective asset accounts, the cash and bank balances in the Cash Book, the stock to the Stock Account, the value of the motor vehicles to the Motor Vehicles Account and the debts due to the respective debtor’s accounts. The liabilities are posted to the credit of the respective accounts and the capital to the credit of the Capital Account – to show the amount invested in the business by the owner and the extent the business is indebted to him. The appropriate folio numbers are, of course, inserted.

The entries in the ledger accounts are usually described in the narration column as ‘balance’ as they usually represent the balances of accounts brought down from the previous period.

These items having been posted, the books are ready for the subsequent transactions to be entered as and when they occur. In examination tests, students may be required to prepare the opening entries and also record the subsequent transactions. The procedure described above will then have to be done before the transactions are recorded.

Evaluation

- Simplified and Amplified Financial Accounting Exercise 3X and 7X

Reading assignment

- Business Accounting 1. Page 232 – 239

- Simplified and Amplified Financial Accounting. Page 127 – 133

General evaluation

- Business Accounting 1. Exercise 25.1 and 2A

- Simplified and Amplified Financial Accounting. Exercise 5, 6 and 8X

Weekend assignment

- Which of the following accounts belong to the purchases ledger (a) bank (b) creditors (c) salaries (d) debtors

- The statement which shows the financial position of a business at a given point in time is (a) trial balance (b) cash book (c) bank statement (d) balance sheet

- The drawings account of a sole trader is transferred to the (a) trading account (b) profit and loss account (c) capital account (d) discounts account

- The salary of a shopkeeper who sells goods would be charged in the (a) Balance Sheet (b) Sales Account (c) Trading Account (d) Profit and Loss Account

- Capital is the (a) money owed by a business to others (b) money owed to a business by others (c) liability of the business to its proprietor (d) total of the long – term liabilities.

Theory

- What is a Journal Proper

- Enumerate eight uses of the Principal Journal

- Explain four differences between a trial balance and a balance sheet.

We hope you enjoyed the class.

Should you any further question, feel free to ask in the comment section below and trust us to respond as soon as possible.