Back to: BUSINESS STUDIES JSS1

Welcome to class!

In today’s class, we will be talking about the journal. Enjoy the class!

Journal

Meaning of journal

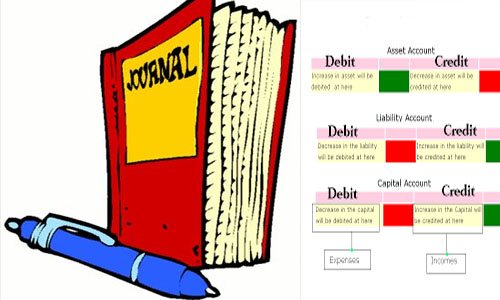

The journal is a book of original entries or prime entries, which recorded transaction in chronological order that is a day by day recording of transactions arranged according to when something happened. Journal can equally be referred to as a daily record into which transactions are entered and classified as debit DR and credit CR before they are posted to the ledgers. The journal has columns for date particulars, folio, debit and credit. The entries are recorded and explanation will be given to show the nature of the transactions, this is referred to as narration.

Advantages of journal

- Its main purpose is to provide a convenient record of a transaction in chronological order.

- The explanations of the entries are made known by the journal.

- It reduces the risk of omission of transactions.

Uses of journal proper

- Opening entries

- Closing entries

- Transfer between accounts.

- Purchase of fixed asset n credit

- Correction of errors

- Sales of a fixed asset on credit

- To answer questions on double-entry principle

Classes of entries

The entries in the principal journal may be composite or simple.

- Composite entries: There may be several accounts to be debited and only one account to be credited and vice versa.

- Simple entries: Only two accounts are involved, one account will be debited and another credited.

Types of journal

The following are the types of a journal;

- Sales journal or sales daybook: This is used for making an accurate recording of credit sales prior to their being posted to the credit sales account.

- Purchases journal or purchases daybook: This is used for making an accurate recording of goods bought on credit prior to their being posted to the debit purchases account.

- Returns inward journal or returns inward daybook: This is used for making an accurate recording of goods sold to customers of which some of them are to be returned to the supplier. The document used for such returns is the ‘credit note’.

- Returns outward journal or returns outward daybook: This is used for making accurate recordings of goods bought but are to be sent back or returned to the supplier as a result of one defect or the other. The document used for such is called called ”debit note”.

- Principal journal or journal proper: This is a book where all transactions that cannot be properly accommodated in any of such as purchases, sales, and return outward or return inward journals are recorded. This is also known as general journals. Examples of such transactions that are recorded in principal journals or proper journals are:

- Opening and closing entries.

- Purchases of an asset.

- Entry adjustment in accounts.

- Writing off bad debts depreciations.

In our next class, we will be talking about Double Entry Bookkeeping. We hope you enjoyed the class.

Should you have any further question, feel free to ask in the comment section below and trust us to respond as soon as possible.